Table of Content

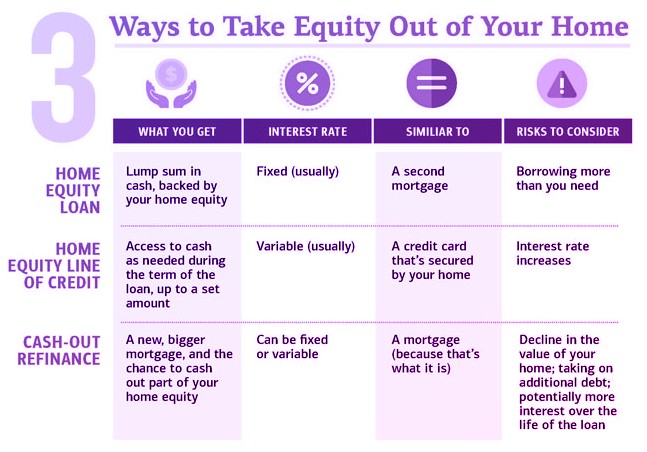

HELs have a number of benefits compared to a HELOC, including a fixed rate and no annual fees. And unlike a HELOC, a HEL will provide loan proceeds as a lump sum. Your lender will provide you with options for accessing your funds. Most allow you to withdraw cash by online bank transfer or a HELOC account card .

After several years of making interest-only payments, the jump to full interest and principal payments can come as a shock, so make sure you review your loan documents and make note of when your HELOC will enter repayment. “Be prepared to make that full payment when the loan converts to a fully amortized payment schedule,” says Tabitha Mazzara, director of operations with the Mortgage Bank of California . The draw period is the predetermined length of time you can use your revolving line of credit. During the draw period, you can withdraw from your HELOC account to pay for any expenses you may have. Made interest-only payments, the principal balance remains the same through the term of the account.

You can make more than minimum payments if you want to

A closed-end line of credit allows borrowers to take out money over a specified period of time, after which it must be repaid in full. When the draw period is over, the payments due on a HELOC will skyrocket if no payments were made to the principal during the draw period. Use our Rate Calculator to find the rate and monthly payment that fits your budget. Understanding your options and obligations with a HELOC is an important step to getting on a solid financial footing. Be sure to calculate what you may owe before your draw period ends, so you’re not stretched financially.

But if you get the disclosure form and the two copies of the notice before or after the closing, Day One begins on when the last of the three things happened. So if the closing happens on a Friday, and if that was the last thing to happen, you have until midnight on Tuesday to cancel. But if you received your Truth in Lending disclosure form on Thursday and you closed on Friday, but didn’t receive two copies of the right to cancel notice until Saturday, you have until midnight on Wednesday to cancel. For cancellation purposes, business days include Saturdays but not Sundays or legal public holidays. Before you sign, read the loan closing papers carefully.If the loan isn’t what you expected or wanted, don’t sign. You also generally have the right to cancel a home equity loan on your principal residence for any reason — and without penalty — within three days after signing the loan papers.

Refinance the Balance Into Your Primary Mortgage

Before you fill out your application, make sure you know the terms of a HELOC and understand it’s fundamental aspect—the draw period—to know if it’s right for you. The draw period length depends on your HELOC’s exact terms and conditions. Generally, the draw period lasts between five and ten years. After the draw period is over, you will no longer be able to withdraw any funds from your HELOC.

You get the loan for a specific amount of money and it must be repaid over a set period of time. You typically repay the loan with equal monthly payments over a fixed term. If you don’t repay the loan as agreed, your lender canforeclose on your home. Unlike some other forms of credit, such as personal loans or home equity loans, most HELOCs have variable interest rates.

Repaying your home equity line of credit

Fixed interest rates and relationship discounts for qualified customers. Gina LaGuardia has more than 25 years of experience in senior editorial roles, and is an expert in personal finance topics, including banking and lending. She has created content for financial powerhouses such as Chase Bank, American Express Canada, First Horizon Bank, BBVA, and SoFi. Get all of our latest home-related stories—from mortgage rates to refinance tips—directly to your inbox once a week. The attached interagency guidance encourages credit unions to work with borrowers where possible, consider sound risk management principles, and minimize risk while meeting the needs of your members. The date you can no longer access funds from your home equity line of credit.

Unlike a HELOC, a home equity loan is an installment loan repaid in fixed payments over time; you can use it to pay off the HELOC and then pay off the home equity loan. Paying off the HELOC in full before the draw period ends is the best option, leaving you with zero balance at the end of the loan. Review your budget looking for places you can cut costs and save money to put toward the HELOC balance. To avoid unpleasant surprises, make sure you understand your HELOC's terms and exactly when the draw period ends. Once the HELOC closes, you can no longer draw from it—and you'll start making larger loan payments.

As an alternative to including this statement, creditors may provide an itemization of such fees with the early disclosures. Any itemization provided upon the consumer's request need not include a disclosure about property insurance. When you’re approved for a HELOC, you will also be approved for a credit limit based, in part, on how much equity you have in your home. You can use this line of credit during what is called the “draw period.” This is the amount of time you have to draw funds from the HELOC. The draw period typically lasts for a fixed amount of time. It can vary between lenders, but the period usually can last up to ten years.

A creditor may not include a general provision in its agreement permitting changes to any or all of the terms of the plan. For example, creditors may not include “boilerplate” language in the agreement stating that they reserve the right to change the fees imposed under the plan. In addition, a creditor may not include any “triggering events” or responses that the regulation expressly addresses in a manner different from that provided in the regulation. Similarly a contract cannot contain a provision allowing the creditor to freeze a line due to an insignificant decline in property value since the regulation allows that response only for a significant decline. A creditor may terminate a plan and accelerate the balance if there has been fraud or material misrepresentation by the consumer in connection with the plan.

Never work with a lender who wants you to lie on a financing application — like saying your income is higher than it really is. Avoid a lender who wants you to apply to borrow more than the amount you need. It’s Cyber Security Awareness month, so the tricks scammers use to steal our personal information are on our minds. If there’s one constant among scammers, it’s that they’re always coming up with new schemes, like the Google Voice verification scam. ☉Credit score calculated based on FICO® Score 8 model. Your lender or insurer may use a different FICO® Score than FICO® Score 8, or another type of credit score altogether.

At Bankrate we strive to help you make smarter financial decisions. While we adhere to stricteditorial integrity, this post may contain references to products from our partners. Matthew Goldberg is a consumer banking reporter at Bankrate.

The disclosures could be located on the same Web page as the application without necessarily appearing on the initial screen, immediately preceding the button that the consumer will click to submit the application. Bankrate is compensated in exchange for featured placement of sponsored products and services, or your clicking on links posted on this website. This compensation may impact how, where and in what order products appear. Bankrate.com does not include all companies or all available products.

If paying only the minimum periodic payments may not repay any of the principal or may repay less than the outstanding balance, a statement of this fact, as well as a statement that a balloon payment may result. A balloon payment results if paying the minimum periodic payments does not fully amortize the outstanding balance by a specified date or time, and the consumer must repay the entire outstanding balance at such time. Once HELOC draw periods expire, borrowers start paying down the money they drew. Also, during HELOC repayment, lenders may allow their borrowers to draw up to the amounts by which they've reduced their principal balances. Reducing a HELOC's $15,000 principal balance to $5,000 would give you $10,000 in funds you could borrow and so on. However, any additional money drawn from a HELOC during repayment is added to the loan, with a likely increase in payment the result.

Personal loan

A Home Equity Line of Credit has two different periods, a draw period and repayment period. The draw period is 10 years, where you have ongoing access to available funds and can use the funds how you'd like. During the draw period, you have the option to select a minimum monthly payment of either 1% or 2% of the outstanding balance, or interest only for those who qualify. Once the draw period ends, the account enters the repayment period.

The repayment period can typically last from 10 to 20 years, depending on the lender. Your monthly payment will likely increase as you start paying back the balance with interest. Once the repayment period begins, the line of credit can't be accessed for new credit advances. The life of a HELOC is split into a draw period, lasting five to 10 years, followed by a repayment period, which can be up to 20 years. If there’s a chance you’ve missed the notification, call or visit your bank in person to review the HELOC terms and get answers to any questions you may have.

No comments:

Post a Comment